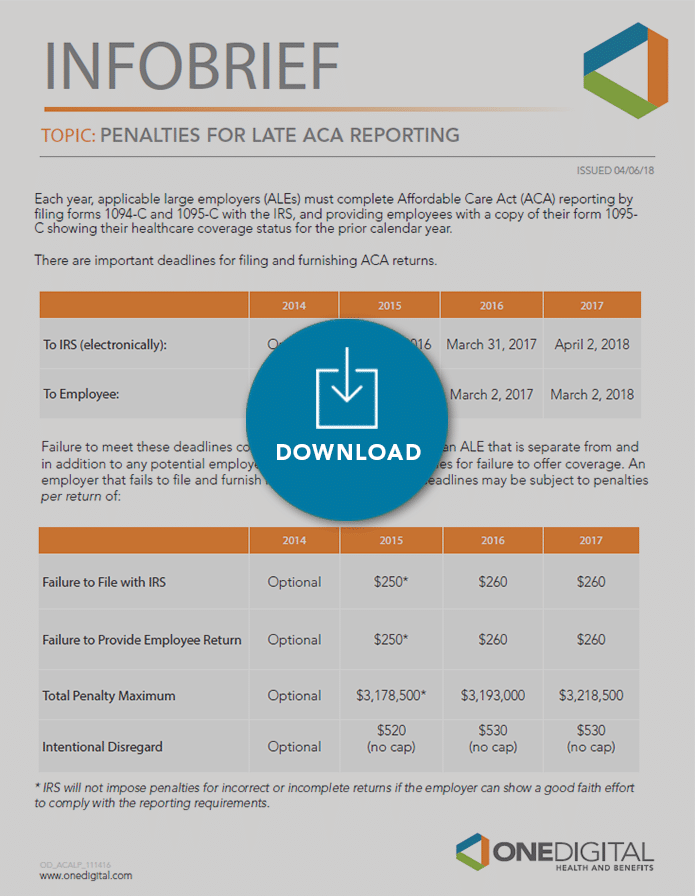

Each year, applicable large employers (ALEs) must complete Affordable Care Act (ACA) reporting by filing forms 1094-C and 1095-C with the IRS, and providing employees with a copy of their form 1095-C showing their healthcare coverage status for the prior calendar year.

There are important deadlines for filing and furnishing ACA returns.

2018 |

2017 |

2016 |

2015 |

|

To IRS (electronically): |

April 1, 2019 | April 2, 2018 | March 31, 2017 | June 30, 2016 |

To Employee: |

March 4, 2019 | March 2, 2018 | March 2, 2017 | March 31, 2016 |

Failure to meet these deadlines could result in costly penalties for an ALE that are separate from and in addition to any potential employer shared responsibility penalties for failure to offer coverage. An employer that fails to file and furnish returns by the applicable deadlines may be subject to penalties per return of:

2018 |

2017 |

2016 |

2015 |

|

Failure to File with IRS |

$270 | $260 | $260 | $250* |

Failure to Provide Employee Return |

$270 | $260 | $260 | $250* |

Total Penalty Maximum |

$3,275,500 | $3,218,500 | $3,193,000 | $3,178,500* |

Intentional Disregard |

$540 (no cap) | $530 (no cap) | $530 (no cap) | $520 (no cap) |

* IRS will not impose penalties for incorrect or incomplete returns if the employer can show a good faith effort to comply with the reporting requirements.

These penalties may be reduced to $50 per return when errors are corrected within 30 days. If, however, reporting is more than 30 days late, or perhaps even several years behind, it is important to consider whether the employer intentionally disregarded the requirements because the penalties are higher and have no caps when intentional disregard is involved.

Intentional disregard occurs when the employers knew or should have known of the requirements but consciously chose not to provide the statement or recklessly disregarded or ignored the duty to provide the statements timely and correctly.

In determining the assessment of penalties, the IRS will look to whether the employer corrected the failure promptly after discovery. Accordingly, if an employer is late completing its ACA reporting, the employer should prioritize correcting any issues and failures with ACA reporting as soon as possible to demonstrate a good faith effort to comply with the requirements. While this may not remove all risks for potential penalties, it will position the employer in a more favorable light with the IRS for reduced penalties.

DOWNLOAD THE INFOBRIEF: Penalties for Late ACA Reporting

Contact your OneDigital representative for questions regarding the deadlines for form 1095-C.

Share

Want to learn more about OneDigital?

Connect with a OneDigital expert today.