Auto-Features That Should Be Added to Your Retirement Plan Today

Author

As the world becomes more automated, many employees also favor auto features in their workplace retirement plan.

In response, many organizations are integrating these auto features to help employees save more efficiently and prepare for retirement with greater confidence. Research show that plans with auto-features have an advantage in terms of participation and contribution rates over plans with no auto features.[1][2] Below are some of the most common and widely utilized auto-features that you should consider implementing within your plan.

Key Automated Features

Auto-Enrollment

Auto-enrollment is when employees are automatically entered into their employer’s retirement plan. When enrolled, employees automatically contribute a specified amount into their account from each paycheck. This is called the default contribution rate and is specified in the plan document.

Participants are now more receptive to higher default contribution rate than ever before. 61% of plans with auto-enrollment have a default contribution rate of 4%, which is a significantly higher than 25% of plans two decades earlier.[3] These higher rates offer employees a valuable opportunity to build their retirement savings.

Additionally, employers must establish a default investment option for employees who do not make their own selection, ensuring contributions are invested in a designated fund.

Employers are required to set up a default investment for their employees who do not make an election decision. Therefore, employees are not only automatically enrolled into the retirement account, but their funds are also automatically invested in a predetermined investment by the plan.

Re-enrollment

Employees who opt out of initial enrollment may not ever reengage with the plan. Implementing a re-enrollment feature can help re-engage these individuals. Annual re-enrollment periods provide another opportunity for employees who previously opted out to participate and allow current participants to review and adjust their contribution rates.

Auto-Escalation/Increase

Auto-escalation is a retirement plan feature that regularly increases an employee's contribution amount. Commonly escalation within a plan is done on an annual basis. Increasing just one percent every year can result in thousands upon thousands of dollars more at retirement through the power of compounding.

Benefits of Compounding

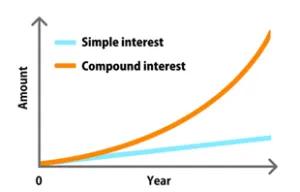

All automatic features look to accelerate the advantage of compounding interest. Compounding occurs when an account’s earnings are reinvested to generate additional earnings over time, allowing both the initial investment and reinvested earnings to grow. The benefit of compounding is that the account will grow from both the initial investment and the additional earnings being reinvested. The earlier employees begin saving, the greater their potential for retirement savings to compound and grow.

Below is a graph that illustrates the advantage of compound interest and how it can be much greater than simple interest. An employee may lose out on significant potential earnings by only gaining interest from the initial investment.

For illustrative purposes only, investing involves risk and there is no guarantee of profit and you can lose some of all of your investment.

Employees Are Ready for Automationn

As technology gets better and the world becomes more automated, it's crucial to stay ahead of the curve. Employees are ready for this transition and stand to benefit from the increased convenience and improved savings outcomes that automated plan features provide. By incorporating the automated features outlined above, you can help your employees work towards stronger retirement outcomes.

To learn more about plan features and ensure your plan aligns with current benchmarks, check out our fiduciary academy session, “Benchmarking Your Plan: The Power of Asking the Right Questions.”

Investment advice offered through OneDigital Investment Advisors.

Sources:

[1]PLANADVISER, “Automatic Plan Features Help Participants Savings Rates Stay Resilient in 2024, Says Vanguard”

[2]PSCA, “Automatic Features Have Tripled in Use Since 2007”

[3]Vanguard, “How America Saves 2025”

ID: 00296833