Markets in Focus: Strength Through Uncertainty

Author

Volatility and uncertainty were the main themes that investors faced throughout the 2nd quarter, beginning with the Liberation Day tariff announcements on April 2nd and ending with the United States getting involved in the conflict between Israel and Iran in the Middle East.

Market Performance

Market performance in the 2nd quarter was strong but volatile. The S&P 500 hit a low point for the year on April 8th, just a few days after the start of the 2nd quarter and President Donald Trump's announcement of reciprocal tariffs. Since then, equity markets have recovered to positive territory for the year. In fact, the S&P 500 and NASDAQ both had their best monthly performance since November 2023 in May.

As of June 30th, the S&P 500 (which represents 500 large-cap U.S. stocks) was up 6.1% year-to-date, while the tech-heavy NASDAQ was up 5%. International stocks, represented by the MSCI EAFE index, outperformed U.S. stocks, rising 19.5% year-to-date. Emerging market stocks, similarly, have outperformed U.S. stocks, ending the quarter up 15.9%.

The U.S. bond market had another positive quarter, though returns were muted compared to the increase in equities. The Bloomberg U.S. Aggregate Bond index, a broad measure of the U.S. investment-grade bond market, rose 1.2% during the quarter to stand at a 4% positive return at the halfway point of the year. The high yield bond index performed slightly better and is now up 4.7% year-to-date.

Finally, the Energy sector experienced difficulties as the price of oil dropped more than 10% in the second quarter after a relatively flat Q1. This decline was blamed primarily on an oversupply of oil in the market as OPEC+ began to phase out their voluntary production cuts in April. Middle East tension escalation or de-escalation could materially alter oil’s trajectory as we move forward.

Economic Growth

Growth of the U.S. economy stalled in the 1st quarter when GDP contracted by 0.2%. However, that negative number was impacted significantly by a surge of imports during Q1 as corporations successfully imported as much as possible before tariffs were announced. Imported goods increased by 51% over the volume in Q4 2024, which was a significant drag on the net export component of the GDP calculation.

Fortunately, growth seems to be returning to normal in Q2. While the first official reading hasn’t been released yet, the Atlanta Fed produces a frequently updated estimate called GDPNow, which estimates growth in the 2nd quarter of around 2.6% as of July 9th.[1]

Tariffs

As mentioned in our last quarterly update (link to last Markets in Focus), one of the largest uncertainties that markets faced was around the plans for tariffs from the second Trump administration. One of President Trump’s primary campaign promises was an increase in tariffs to level the playing field for U.S. companies regarding global trade. During his inaugural address, he again promised to “tariff and tax foreign countries to enrich our citizens.” [2]

Between the inauguration and the end of March, most of the tariff focus was on Mexico, Canada, and China. This included increasing the tariffs on Canada and Mexico to 25% and increasing tariffs on Chinese imports to 20%. The new tariffs were later paused, and some items were exempted from tariffs, such as components that go into the production of automobiles after speaking with leaders from U.S. automakers.

However, the most impactful tariff announcement came on April 2nd, which Trump called Liberation Day, when his long-promised “reciprocal” tariffs were announced. This included a baseline minimum of 10% tax on imports from all countries, and even higher tariff rates for countries where the U.S. has a high trade deficit. This took the markets by surprise as some of the tariff rates were much higher than expected, including 20% on imports from the European Union, 25% on South Korea, and 32% from Taiwan.

What remains unclear is the ultimate goal of the new tariff policy in the United States. On the one hand, the administration could be looking at tariffs to increase government revenues, which could offset some of the tax cuts Trump also promised. Or, they could be used as a negotiating tactic to try to get concessions from other countries on policies such as curbing illegal immigration and the illegal importation of fentanyl. What was telling was the results of the first trade agreement that was signed with the U.K., a country with which the U.S. has a trade surplus (meaning we export more than we import). Even though they were the first to finalize a new trade agreement, the 10% minimum tariff rate remained in place, indicating a desire to grow the revenue of the U.S. government. This was reinforced by the upcoming trade deal with Vietnam, which will include a 20% tariff. Generating a larger amount of revenue from foreign trade would be a significant shift in fiscal policy.[3]

Geopolitics

Further fueling uncertainty in markets was the spark in hostilities between Israel and Iran. On June 13th, Israel launched an offensive against Iran over the threat of developing a nuclear weapon. The military operation, called Operation Rising Lion, included over 200 aircraft striking nuclear, military, and strategic sites across Iran. Iran responded by firing more than 150 ballistic missiles and over 100 drones at Israel, most of which were intercepted by Israel’s Iron Dome.

The conflict escalated over the next 9 days until June 22nd, when the United States launched air strikes on additional Iranian military targets and nuclear sites. Fortunately, after a brief retaliation against a U.S. base in Qatar, all sides agreed to a cease-fire 2 days later.

The conflict, however brief, still has a tremendous humanitarian impact as innocent civilians were caught in the crossfire. Given the flare-ups in the region and the continued conflict between Ukraine and Russia, it’s important to acknowledge that geopolitical risks exist throughout the world. Fortunately, while there have been numerous conflicts in the Middle East over the past 30 years, none of them have had a significant impact on broad U.S. markets.

Fiscal Policy

One of the biggest and most impactful events of the 2nd quarter came in the passing of the budget mega-bill in Congress and signed by President Trump. The bill passed the House of Representatives by a single vote and passed the Senate because of a tie-breaking vote by Vice President J.D. Vance.

The bill covered an extremely broad array of policies that were highlighted by the extension of the 2017 Trump tax cuts that were set to expire at the end of this year. Trump was also able to fulfil some of his campaign promises, such as eliminating taxes on overtime and on tips. The bill also increased the U.S. military budget by $150 billion, and increased funding to Immigration and Customs Enforcement (ICE) by $100 billion.

The other side of the bill was the cuts that were made, including critical cuts to Medicaid and food assistance programs.

According to preliminary analysis by the Congressional Budget Office (CBO), the bill, as passed, would increase government deficits by $3.4 trillion between 2025 and 2034.[4] This calls into question the sustainability of the government to continue to add to its debt.

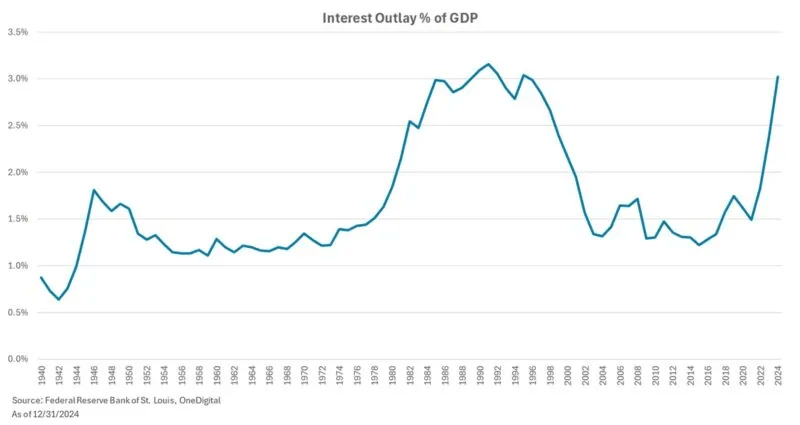

One metric to keep an eye on is the amount of interest that the government is paying on its debt as a percentage of GDP. The U.S. government is in a position where that percentage hasn’t been this high since the mid-1990s. If the government is going to continue to operate at a deficit, the only way that can be brought back down is to either decrease interest rates or grow the economy (measured by GDP) at a faster rate.

Fed Uncertainty

Another way to look at deficit spending in fiscal policy is that it tends to be inflationary. The Federal Reserve, which controls monetary policy, has a dual mandate – to maintain price stability (a reasonable level of inflation) while maintaining maximum sustainable employment.[5] It does this primarily through setting the overnight lending rate, which sets a baseline for many other interest rates around the economy.

Estimates coming into 2024 were that the Fed would lower interest rates twice during the year. Inflation had been moderating (though not yet back to the 2% target), and there were signs that the job market may have been softening. However, to this point, the Fed has held off on any cuts over fears that inflation may re-accelerate due to the tariff announcements and continued deficit spending.

According to current market sentiment, the estimate is that there will still be two cuts this year, with the first coming at the September 17th meeting of the Federal Open Market Committee (FOMC), and the second coming at the following meeting on October 29th.[6]

Looking Ahead

The Investment Team at OneDigital continues to look at the following key economic risks through the end of the year:

Risk 1: Impact of U.S. Tariffs and Trade Tensions:

The implementation of broad and reciprocal tariffs by the United States poses a significant downside risk to the U.S. economic outlook for the remainder of the year. The tariffs outlined in early April could lead to substantial disruptions in how trade occurs on a global scale, resulting in increased costs for businesses through higher import duties, which could pass through to consumers in the form of higher-priced goods. Estimates suggest that these tariffs could have a material negative impact on U.S. GDP growth and could also contribute to increased inflationary pressures. Furthermore, the likelihood of other countries increasing their tariffs on U.S. goods imports could further escalate trade tensions and worsen the negative consequences for international trade. The prospect of a full-blown trade war scenario represents a significant threat to the stability and growth of the U.S. economy.

Risk 2: Persistent Inflation or Stagflation Concerns:

Despite the slow moderation in inflation during the first quarter of 2025, inflation rates in the U.S. remain stubbornly above the Federal Reserve's target. This persistence of higher-than-target inflation raises concerns about the potential for stagflation, a challenging economic condition characterized by a combination of high inflation and slow economic growth. The risk of stagflation is particularly concerning because it presents a dilemma for policymakers, potentially requiring trade-offs between controlling price increases and supporting economic activity. The cautious approach adopted by the U.S. Federal Reserve regarding interest rate cuts reflects these concerns. The potential for tighter monetary policy in response to persistent inflation could dampen economic growth by increasing borrowing costs and reducing investment and consumer spending.

Risk 3: Potential for Economic Slowdown:

Beyond the risks associated with tariffs and inflation, there are concerns about a broader economic slowdown in the U.S. Factors such as slowing consumer spending, cautious corporate investment, and the lingering effects of higher interest rates could contribute to a more pronounced economic slowdown than currently anticipated by some forecasts. Such a slowdown could negatively impact corporate earnings, employment, and overall market sentiment.

Want to gain a deeper understanding of tariffs and their impact on the economy? Check out our blog post, “Understanding Tariffs: Their Mechanisms, Motivations, and Impacts.”

Sources:

[1]Federal Reserve Bank of Atlanta, “GDP NOW”

[2]PBS News, “A timeline of Trump’s tariff actions so far”

[3]BBC, “Trump signs order confirming parts of UK-US tariff deal”

[4]Congress Budget Office, “Information Concerning the Budgetary Effects of H.R.1, as Passed by the Senate on July 1, 2025"

[5]Federal Reserve Bank of Chicago, “The Federal Reserve’s Dual Mandate”

[6]CME Group, “FedWatch”

___________

Investment advice offered through OneDigital Investment Advisors LLC. The materials and the information provided are not designed or intended to be applicable to any person's individual circumstances. These statements do not constitute an offer or solicitation in any jurisdiction. Any reference to a specific company is not a recommendation to buy, sell, or hold any security. Any economic forecasts in this commentary are merely opinion, and any referenced performance data is historical. Past performance is no guarantee of future results. All investment involved risk of loss. Some information has been obtained by sources we believe to be reliable. OneDigital Investment Advisors LLC makes no representations as to the accuracy or validity of this information. Additionally, OneDigital Investment Advisors does not have any obligation to provide revised investment commentary in the event of changed circumstances. Views and Opinions expressed herein are provided as of April 11, 2025.

ID:00252905