Q4 2022 Markets in Focus: Is The Hot U.S. Labor Market Finally Turning Around?

Author

Economists are scratching their heads more than usual, as the global marketplace is experiencing a new regime shift with various economic inflection points and monetary policy changes.

A steady drumbeat of data suggests that the U.S. Federal Reserve rate hikes are starting to bite into the real economy. As the economy reels into late cycle slowdown, investors are asking important questions: How long will inflation run hot? How high will the interest rate reach? And, most importantly, is the hot U.S. labor market finally turning around?

Anecdotes suggest so, but recent data continue to show a labor market where firms are holding on to existing workers, and those who lose jobs can find new ones quickly. Data and arguments also suggest the labor market is still too strong to allow the Fed to pivot away from its tightening strategy.

On the other hand, the demand for labor is starting to show signs of cooling, which indicates the job market could be much cooler by early next year, giving the Fed space to end its current aggressive tightening cycle.

After the market cheer during the Pandemic and record-breaking stimulus, the inevitability of soft-landing amid spiraling inflation and policy tightening now begs the question if we’re (or soon will be) in a recession. Followed by the more important question about how long and severe it will be.

Americans are seeing some signs of positive progress relative to the struggles that other parts of the world are experiencing.

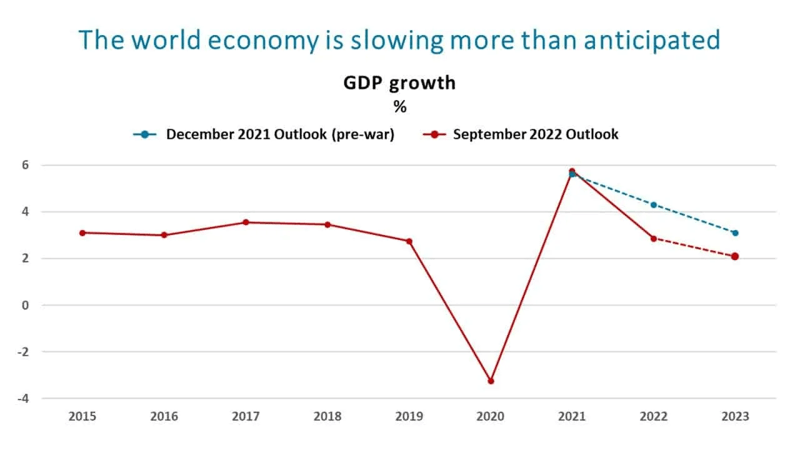

Global real gross domestic product (GDP) stagnated in the second quarter of 2022, and output declined in the U.S. and many other leading countries. With recent indicators taking a turn for the worse, the global economic outlook is darkening.

For investors with money in the markets, it’s been tough to watch the drops for the last few months. The advice has been not to make any sudden moves, as selling after decreases is generally a bad idea. Case in point, if investors pulled money out of the markets following the dips in September, they’d have missed out on some of the ups we’ve already had in October. As we move into the fourth quarter, investors continue to question whether they’re seeing a recovery, the onset of a bull market, or if this is simply a bear market rally. Most agree—it’ll be a while longer before we know for sure if the Fed’s policies have had the intended effects.

Here’s What We Know

The third quarter threw a lot at us. The Fed hiked interest rates with three increases of 0.75% in a row, including two in the third quarter alone. Inflation (headline consumer price index, or CPI) remained high at 8.3% after reaching 9.1% at the end of the second quarter—it’s highest mark in the last 42 years.

Fear of a recession and central bank tightening continued to drive market volatility in the third quarter. This fear has led to a tough first nine months of the year, with global equities down around 25% and the Bloomberg Global Treasury benchmark sliding 20% as of the end of September. The Standard & Poor's 500 Total Return Index was down 9.22% in September, bringing its year-to-date return to -23.88%. Barclays U.S. Aggregate Bond Index posted -4.32% and -14.61% for the same periods, respectively.

Meanwhile, the U.S. dollar (USD) surged and currency fluctuations squeezed a number of Asian economies and Great Britain. Never before in history has the U.S. dollar's value been so close to the pound, and the news generated a sense of emergency for the U.K. central bank.

The Fed’s aggressive monetary tightening poses an economic threat to the rest of the world. However, the central bank is committed to driving inflation back down to the long-term target of 2%. That leaves investors wondering how much collateral damage will occur in the process.

According to a recent statement from United Nations, “excessive monetary tightening could usher in a period of stagnation and economic instability.” The Fed must do what’s best for the United States, but it may mean inflicting stress on the rest of the world, in large part by bolstering the U.S. dollar. This stress raises the price of imports in other countries, stoking inflation and forcing central banks to respond with matching rate hikes.

Developing countries may face even harsher effects, including foreign investments leaving out of the country and the burden of paying higher interest on dollar-denominated debts. Nevertheless, the Fed is attempting to follow the congressional mandate to achieve price stability balanced with maximum sustainable employment.

The pace and magnitude of the Fed tightening could also hurt the labor market and increase the risk of policy error. It could lead to economic stagnation and potentially a recession by the second half of 2023. Investors have already experienced disappointing returns and unsettling market volatility. Plus, the positive correlation between risk-free and risky assets has diminished the benefit of portfolio diversification between stocks and bonds.

The September jobs report remained strong with a headline payroll increase of approx. 263,000 and a 3.5% unemployment rate. Growth in average hourly earnings remained at a monthly pace of 0.3%, meeting consensus estimates. Although this data indicates the labor market is not cooling enough to give the Fed a reason to pivot, some cracks have appeared in hiring and job growth, with the number of job openings declining by 1.1 million in August. There were 1.67 job openings for every unemployed American, down from 1.97 in July. The unemployment rate decreased in September, yet hiring is slowing, and labor participation has declined. Layoffs are not yet pervasive, but we expect them to increase and may result in increased unemployment in the future. The softening of the labor market is one of many reasons why the Fed may consider putting the brakes on raising interest rates.

What’s Ahead?

Overall, 2022 has been a lackluster year for the world economy. The year started with the headwinds of Russia’s invasion of Ukraine. Global growth slowed significantly with the generalized tightening of monetary policy to counteract the high inflation that has persistently stayed above targets. And this, combined with China’s zero COVID-19 policy and a potential downturn in housing market due to soaring borrowing costs, could take the global growth for the year down to 3%, according to an Organisation for Economic Co-operation and Development (OECD) estimate. This estimate is far below expectations of a recovery-led growth of 4.7% at the start of the year.

Compared to OECD forecasts from last year, before Russia’s aggression against Ukraine, global GDP is now projected to be at least $2.8 trillion lower (USD) in 2023.

Here are some of the other highlights:

- The earnings outlook for the fourth quarter isn’t good. Analysts decreased the Earnings Per Share estimates in aggregate for the fourth quarter by 4.5% (to $58.01 from $60.73) from June 30 to Sept. 29.

- The global economy is in a sustained slowdown. We are likely to see higher volatility in the markets, and both equities and bonds may continue to trend downward, in a sustained bear market. However, there could be some interim recovery. Traditionally there’s a period after the fall when markets bounce around for a while before breaking through.

- The Fed is under pressure to stop raising interest rates for fear that it may plunge the world economy into recession. Nevertheless, the Fed must be firm to bring down inflation to avoid the risk of exacerbating the pain it seeks to mitigate. And, because it takes time to see the effects of the Fed’s actions, it’s likely next year before we see the breakthrough.

- No more soft landing. Most economists project a recession in the second half of 2023. However, deeper spillovers from interest rate sensitive sectors (e.g. housing) may bring the risk forward.

What We’re Watching

In the next 12 to 18 months, we’re keeping an eye on a few things as the economy evolves and the Fed continues trying to keep up.

Inflation

- The persistence of inflation is a concern, as high inflation has stuck around longer than anticipated. In many economies, inflation in the first half of 2022 was at its highest since the 1980s. While the peak may have passed, the decline is expected to be painfully slow.

- The Fed’s focus on lowering inflation is not misplaced, but it’s also getting more difficult to bring inflation down as it gets more deeply entrenched in the economy.

- If the Fed does not deliver enough by tightening to curb inflation, it risks entering into an unfortunate period of uncertainty with the financial markets. The Fed will always promise to raise rates to deliver its congressional mandate of price stability, and the markets will always suspect that the Fed will lose its resolve.

Job Markets

- Low unemployment, coupled with the headline payroll increase, indicates that the labor market is still resilient. A tighter monetary policy to control inflation could lead to rising unemployment and lower productivity.

- Former Secretary Lawrence Summers recently said, “We probably have a different kind of labor market, in which there’s going to be more upward pressure on wages at any given level of labor market tightness than there has been historically.”

- Summers expects unemployment needs to climb sharply to attain disinflation, which may justify an inevitable U.S. recession.

Global Changes

- There’s been chaos in England, with tax cuts and bond selling as the pound has taken a horrible dive, all while the central bank is trying to take control and stop inflation.

- The new U.K. prime minister has enforced economic policy that is shredding its credibility with Energy Price Guarantee, unfunded tax cuts, and creating liquidity distress associated with the U.K. gilt yield curve.

- While the strong dollar is good for many (think U.S. importers, travelers, and shipping), it’s causing a crisis in other countries when local currency values drop.

- This year is set to end with a recession in Europe. Europe’s heavy dependence on Russian gas means that retaliation and a large rise in gas prices would almost certainly send the region into a recession.

- And in China, recent lockdowns triggered a significant slowing in economic activity. Now early signs of a reopening have emerged. However, the low level of vaccination among the nation’s elderly means the risk of further lockdowns will continue until the COVID-19 vaccine reaches critical mass.

The Markets

- We believe that slowing core inflation should allow the Fed to go on hold and slow down rate hikes in early 2023. The oversold equity-market sentiment means a lot of bad news is already priced in.

- The treasury yield curve remains inverted, where the spread between the 10-year and the 2-year yield is it’s most negative since Sept. 1981. For more on the yield curve, check out our Markets In Focus post from the second quarter.

- Investors remain worried about high inflation, slowing growth, and the potential for an aggressive Fed to cause a recession.

In times of uncertainty, when markets get volatile, it can be tempting to change course. Each crisis can feel daunting, from geopolitical risks to high inflation and changes in monetary policy. Rather than trying to predict what happens next, keep in mind that trying to time the market is very difficult. Excessive trading can create a whipsaw effect that results in more distress. It’s thus critical for investors to think clearly and plan for volatility.

When faced with uncertainty, investors should:

- Keep things in a historical perspective with a long-term view.

- Stay invested! Remember, “time in the market” is more important than “timing the market.”

- Consider building resilience into your portfolio with effective diversification in alignment with your long-term financial plan.

Investment advice offered through OneDigital Investment Advisors, an SEC-registered investment adviser and wholly owned subsidiary of OneDigital.

Any economic forecasts made in this commentary are merely opinion, and any referenced performance data is historical. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. All investments are subject to risk of loss, and any investment strategy may lose value. Past performance is no guarantee of future results.