Pooled Employer Plans: Benefits for Your Business

Author

Article Summary

Explore how Pooled Employer Plans (PEPs) work, how they compare to traditional 401(k) plans, and why businesses of all sizes are considering them as a potential way to simplify plan management while supporting their employees' retirement readiness.

Nearly half of full-time working Americans still do not have access to a workplace retirement plan. (According to the Economic Innovation Group)1

That statistic matters, and not just as a policy concern. It reflects a real tension many employers are navigating right now.

Employee Engagement and the Retirement Savings Gap

Employees are increasingly asking for more financial support in the workplace. In fact, (84%) believe employers should more actively assist them with their specific financial issues, with retirement preparation among their top priorities.2

Younger workers, in particular, are not just asking, they are actively engaging. PwC reporting that over 79% of younger employees use employer-provided financial wellness programs when available. [3] Yet despite that demand, some employers still hesitate to offer retirement plans at all. According to ShareBuilder 401k, in 2026, 12% of small business owners cited that they believe their employees are not interested in a 401k plan as a reason not to offer a retirement plan.4

That disconnect is important, and worth examining. For many employers, the challenge may not be whether retirement benefits matter to their workforce. The deeper challenge is often the perceived complexity: the fiduciary responsibility, the ongoing administrative workload, and the long-term oversight that comes with sponsoring a plan.

At the same time, employers are under growing pressure to offer competitive benefits, retain talent, and manage rising administrative and fiduciary demands. That combination is driving increased evaluation of Pooled Employer Plans (PEPs) as a potential way to simplify retirement plan management, reduce some of the operational burden, and potentially compete more effectively in the talent market.

What is a PEP?

A Pooled Employer Plan is a retirement plan structure created under the SECURE Act, designed to allow unrelated employers to participate in a single, shared plan arrangement. By pooling resources, participating employers may benefit from greater purchasing power and reduced plan-level administrative complexity, allowing you to spend more time focused on running your business.

Central to the PEP structure is the Pooled Plan Provider (PPP), which generally serves as the plan sponsor and administrator for the pooled arrangement, assuming many of the plan-level responsibilities that would otherwise rest with your organization.

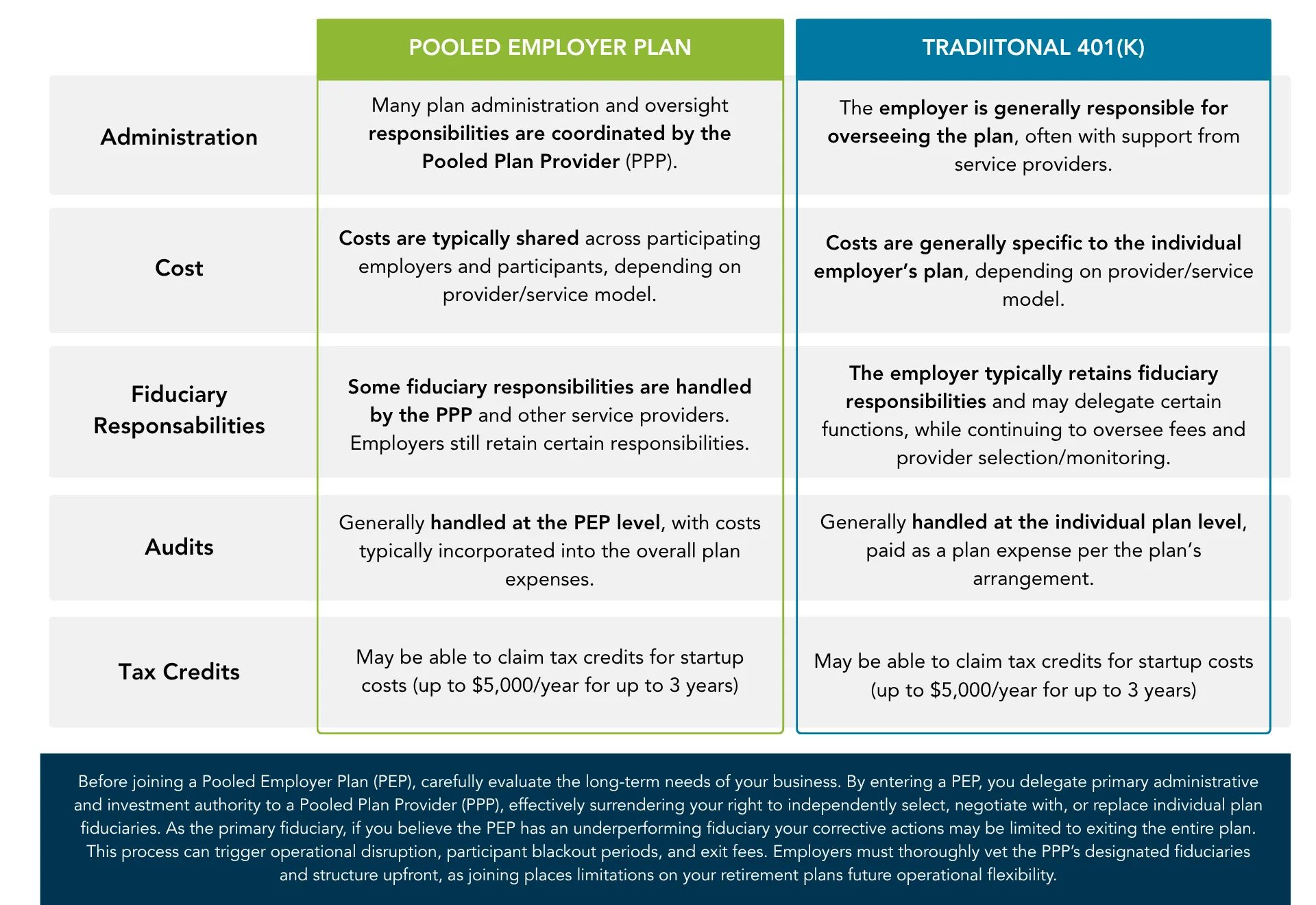

PEP vs. Traditional 401(k)

A retirement plan can be a valuable tool for attracting and retaining employees, but the right structure depends on what your business values most, including how much flexibility, oversight, and administrative responsibility you want to retain internally.

This chart provides a simplified snapshot of common differences between a PEP and a traditional 401(k). The sections below explore what those differences can mean in practice.

-

Administration & Oversight

In a traditional 401(k), your organization typically sponsors the plan and coordinates the day-to-day relationship between providers such as the recordkeeper, TPA, and advisor.

In a Pooled Employer Plan, many of those plan-level administrative functions are centralized through the Pooled Plan Provider (PPP). A PEP may reduce the amount of direct coordination your team manages internally, while a traditional 401(k) structure generally allows you to retain more direct oversight of provider relationships and plan administration.

-

Governance & Fiduciary allocation

In a traditional 401(k), your organization generally retains responsibility for selecting and monitoring providers and investments, although certain functions may be delegated contractually.

In a PEP, the Pooled Plan Provider (PPP) and other named fiduciaries may assume certain plan-level responsibilities, including administrative fiduciary duties under ERISA Section 3(16) and discretionary investment management under ERISA Section 3(38). That said, the adopting employer still remains responsible for prudently selecting and monitoring the Pooled Plan Provider (PPP) and fulfilling any duties retained under the terms of the arrangement.

This structure shifts some fiduciary responsibilities to the pooled provider model, while your organization retains defined oversight responsibilities depending on how the agreement is structured.

-

Economics

Both traditional 401(k)s and PEPs can use a combination of asset-based fees, per-participant charges, revenue sharing, and employer-paid costs. The distinction is less about whether fees exist and more about how pricing is structured and managed.

Traditional plans may offer greater flexibility to negotiate pricing, select providers independently, and determine how costs are allocated between your organization, the plan, and participants. PEPs often use more standardized pricing arrangements designed to simplify cost management across participating employers.

-

Plan Design & Control

Traditional single-employer plans generally offer flexibility around plan design decisions, including eligibility provisions, matching formulas, vesting schedules, investment menus, and provider selection.

PEPs typically operate within a more standardized framework, intended to support consistency across all participating employers. The degree of customization available to your organization will generally depend on the specific Pooled Plan Provider model.

-

Filings & Audits

With a traditional 401(k), your organization is generally responsible for its own Form 5500 filing and coordinating the annual audit process with your providers and auditors.

PEPs typically handle these processes at the pooled plan level through a consolidated filing and centralized audit structure. While adopting employers still maintain certain responsibilities, the administrative work related to filings and audit coordination may be reduced, depending on the Pooled Plan Provider model.

-

Operational Considerations

Traditional plans typically offer greater flexibility to change providers, redesign plan features, or adjust service arrangements over time. That flexibility comes with a trade-off: your team is responsible for managing the logistics, including payroll integration, participant notices, fund mapping, blackout periods, and vendor coordination.

PEPs often use a more standardized onboarding and operational framework, which may simplify implementation for organizations with limited internal resources. Before adopting a PEP, it is important to understand how future changes, transitions, or exits from the arrangement would be handled.

-

Risk & Fit

Neither structure is inherently “better”. Outcomes in both models depend heavily on governance quality, operational discipline, provider oversight, fee transparency, and ongoing monitoring, regardless of which structure your organization selects.

PEPs and traditional 401(k)s differ primarily in how responsibilities are allocated: between your organization and the Pooled Plan Provider (PPP) on one hand, and your internal governance structure on the other. Getting that allocation right, and understanding what your organization is taking on in either case, can make a meaningful difference in both operational efficiency and long-term plan outcomes.

Transitioning to a Pooled Employer Plan

Whether you are converting an existing plan or launching one for the first time, the transition involves important considerations across plan design, payroll integration, investments, participant communications, and fiduciary structure. Working through those details carefully tends to matter, both for how smoothly the process goes and for the experience your employees ultimately have.

Connecting with a OneDigital Retirement Plan Specialist can help you assess your options, understand different provider models, and move forward with a clearer picture of what each path involves.

Looking to learn more about managing a retirement plan? Explore OneDigital’s Fiduciary Academy.

Participation in a Pooled Employer Plan does not eliminate all employer fiduciary responsibilities. Cost savings, administrative efficiencies, and employee participation levels may vary based on plan design, provider structure, and workforce characteristics. Employers should consult with legal, tax, and financial professionals when evaluating retirement plan options.

This article is for informational purposes only and should not be interpreted as specific advice. You should make decisions based on your unique objectives and financial situation. If you are unsure please work with an appropriate advisor to review your specific circumstances. Additionally, any statements made reflect our views and/or opinions and are not intended to guarantee any particular result.

Investment advice offered through OneDigital Investment Advisors LLC. ID: 00589331

[1] The U.S. retirement System: Fast Facts. Economic Innovation Group. https://eig.org/whos-left-out-of-americas-retirement-savings-system/

[2] Morgan Stanley at Work, & Whatley, S. (2025). State of the Workplace 2025 Financial Benefits Study. In State of the Workplace [Report]. https://www.morganstanley.com/content/dam/msatwork/doc/pdfs/state-of-the-workplace-2021/state-of-the-workplace-study-2025.pdf

[3] PricewaterhouseCoopers. (n.d.). 2026 Employee Financial Wellness Survey: PWC. PwC. https://www.pwc.com/us/en/services/consulting/business-transformation/library/employee-financial-wellness-survey.html

[4] Simple, affordable 401K plans built for Small and Medium-Sized businesses | ShareBuilder 401K. (n.d.). ShareBuilder 401k. https://www.sharebuilder401k.com/blog/small-business-retirement-trends-survey-2026