The Retirement Savings Gap for Executives is Real

Author

As corporate cultures and workplace values continue to be redefined, increasingly, more employers are recognizing the need to fortify employee benefit plans and better equip their teams for retirement readiness.

They understand that partnering with employees positions their company competitively to attract and then retain its valued workforce. But many management teams and human resources departments are surprised to learn that they may be underserving their top executives' retirement saving needs when it comes to benefits. Compensation committees may not realize that the deficit exists, and plan sponsors may not have recognized it. Sometimes, even the high-wage earners themselves do not know they face a retirement savings shortfall until it is too late.

The Retirement Savings Gap Reality

Retirement planners often cite 70 to 80% of pre-retirement annual earnings as a target for helping workers determine how much they will likely need in each year of their retirement. At best, this guidance presumes that once retired, individuals will be content to downscale their lifestyle by 20 to 30 percent and will not outlive actuarial table projections. Other variables not factored into these rule of thumb percentages are questions about the stability of the social security system and the impact of economic periods outside predicted margins, such as our current economy, with soaring inflation and eroded purchasing power.

Even if 70 to 80% of pre-retirement annual earnings is an acceptable savings percentage for living comfortably in retirement, it is a target that highly compensated employees (HCEs) may not achieve through the most widely used retirement savings strategies.

Both Qualified Plans and Social Security Benefits Have Limits

Qualified retirement savings plans, such as individual retirement accounts (IRAs), 401(k) plans, and 403(b) plans, all have regulatory limits on the amount workers can save on their own or the employer can contribute. For example, for 2022, the maximum annual pretax deferral contribution to a 401(k) plan is $20,500. Or $27,000 if the worker is over age 50, with a “catch up contribution” of $6,500. Because this rule applies across all income levels, the more the employee earns, the less, by the percentage of compensation, they can save through a qualified plan.

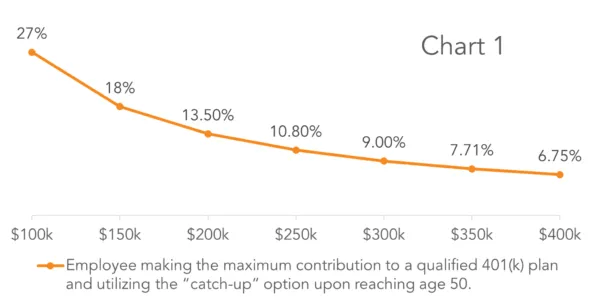

Chart 1 helps illustrate how the retirement saving gap grows wider as an employee’s compensation increases. The employee earning $100,000 on an annual basis will generally be able to save enough through a qualified plan to draw each year of retirement, almost 30% of their pre-retirement annual earnings. In comparison, the employee earning $400,000 annually will only save less than 7% of pre-retirement compensation.

Information is based on 401(k) limits as established by Department of the Treasury, IRS for 2022 and published November 17, 2021. https://www.irs.gov/newsroom/irs-announces-changes-to-retirement-plans-for-2022

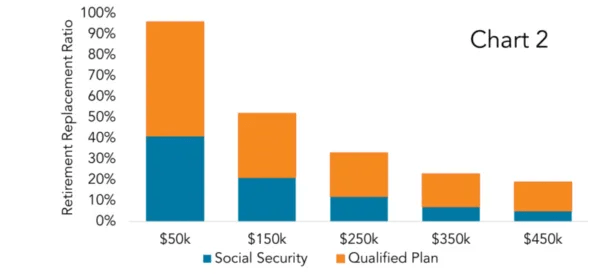

Social security benefits are also a component of retirement savings strategies, but like qualified plans, social security contributions and payouts have mandated limits. Chart 2 shows a broader perspective of how the retirement savings gap grows greater as compensation increases.

The combination of social security benefits (shown in blue) and maximized contributions to a qualified plan will position a retired worker whose salary was $50,000 to draw nearly 95% of this amount in retirement annually. In contrast, social security benefits plus maximized qualified plan contributions will leave the worker who earns $450,000 in compensation to draw upon retirement, less than 30% of their pre-retirement annual earnings.

Assumptions: Employee, age 45, contributes 10% of pretax salary to a qualified plan. Plan sponsor matches $0.50 of the first 6% contributed. The employee’s salary increases 3% per year and contributions up to the maximum allowed by law. Contributions grow tax deferred at 7% annual interest. At age 67, the employee’s account balance is paid out in 4% installments. Values shown include income from Social Security, and historical contributions to a 401(k), but assume no other sources of income. Past performance cannot predict future results. Source: PLANSPONSOR & Prudential: Why Employers Should Care About the Cost of Delayed Retirements.

Although the charts represent generalizations, the big picture message is crystal clear. Highly compensated employees can face a substantial gap in the percentage of compensation they can save for retirement through qualified plans versus the percentage employees at lower earnings levels can save.

Nonqualified Deferred Compensation Plans Can Bridge the Gap

Nonqualified deferred compensation plans (NQDC) can offer an effective strategy for helping highly compensated employees save beyond the limits of qualified plans. Inherently flexible and with no participation or contribution limits, NQDC plans provide participants personalized choices for distribution. Furthermore, because NQDC plans can be designed to be accessible before the participant reaches the age of 59½, they can be an attractive strategy for more than retirement savings, such as funding a child’s college tuition.

Tax-efficient for both the plan sponsor and the plan participants, NQDC plans can help ensure the long-term commitment of a company’s key talent, providing operational continuity. Additionally, plans can be linked to performance objectives and tailored to support specific goals of the organization. By customizing contribution and vesting schedules (measured in phantom stock values), plan sponsors can enable executives to share in increases and decreases in the organization’s valuation, creating an ownership-style experience for the plan participants without any actual dilution of equity rights.

Executive salaries and stock options alone don’t make or keep organizations competitive in today’s marketplace. Executives and top talent rightfully expect the company they represent to partner with them by providing tools for effective, tax-deferred savings plus education to help them personalize their retirement strategy and understand exactly where they stand. The executive benefits team at OneDigital Retirement + Wealth can facilitate the creative design of a nonqualified deferred compensation strategy or evaluate the effectiveness of an existing NQDC plan.

Want to read more about plan design? Check out our recent blog post: Your 401(k) Had Better Shine!

Investment advice offered through OneDigital Investment Advisors, an SEC-registered investment adviser and wholly owned subsidiary of OneDigital.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. You should seek specific advice from your tax professional before pursuing any idea contemplated herein.

Andrew Hart is affiliated with Valmark Securities, Inc. Securities offered through Valmark Securities, Inc. Member FINRA, SIPC. Investment Advisory Services offered through Valmark Advisers, Inc. a SEC Registered Investment Advisor. OneDigital and Fulcrum Partners are separate entities from Valmark Securities, Inc. and Valmark Advisers, Inc.