Affordable Care Act (ACA) Update – New Proposed Rule Simplifying Grandfathered Health Plans

Author

Article Summary

On Thursday, July 15, several Departments issued a new proposed rule aimed at simplifying the ACAs grandfathered plan provisions. Specifically, the Departments, e.g., Internal Revenue Service (IRS), Department of Labor (DOL), Employee Benefits Security Administration (EBSA), Center for Medicare & Medicaid Services (CMS), and Health and Human Services (HHS), present, for consideration, an amendment to the ACA that provides employers, with grandfathered health plans, greater flexibility when making plan changes.

On Thursday, July 15, several Departments issued a new proposed rule aimed at simplifying the ACAs grandfathered plan provisions.

Specifically, the Departments, e.g., Internal Revenue Service (IRS), Department of Labor (DOL), Employee Benefits Security Administration (EBSA), Center for Medicare & Medicaid Services (CMS), and Health and Human Services (HHS), present, for consideration, an amendment to the ACA that provides employers, with grandfathered health plans, greater flexibility when making plan changes. These new provisions allow these employers to make a broader set of plan changes without the fear of losing grandfathered status.

Background

Since taking office, the President has set his sights on improving health care and health care outcomes for Americans. One of the first Executive Orders of the President, EO #13765 issued January 20, 2017, Minimizing the Economic Burden of the Patient Protection and Affordable Care Act Pending Repeal, instructs regulatory agencies to make every effort possible to delay, change, or eliminate any provisions of the ACA that imposes a “cost, fee, penalty or regulatory burden.”

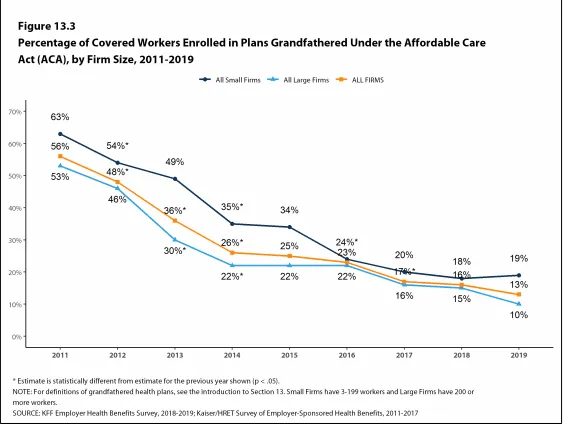

In alignment with that Executive Order, the Departments began looking at grandfathered plans in 2019 since a significant number of these plans were still in existence nine years after the implementation of the ACA. The unanticipated popularity of maintaining these plans drove the Departments to understand this desire and what challenges exist in maintaining these grandfathered plans, i.e., avoiding the loss of grandfathered plan status resulting from the modification of certain plan provision changes. The Departments solicited input in their February 25, 2019 request for information (RFI) specifically seeking to understand the effect that plan changes, made to keep pace with rising health care costs, have on the ability to keep grandfathered status.

Rationale offered by commenters regarding the desire to maintain grandfathered plans includes lower rates than ACA plans with the same or more generous coverage and more robust networks. Additionally, they expressed a desire to modify plans to better keep pace with economic downturns and market dynamics.

Current Grandfathered Plan Provisions

The ACA currently allows employers to maintain their grandfathered plan status if they don’t make significant changes to their health plan or its administration. Plan changes are measured, cumulatively, by comparing the plan provisions existing on March 23, 2010, with the current or proposed plan provision. The loss of grandfathered status takes place on the effective date of the change.

The 2015 final rules on grandfathered status define six types of plan changes that will cause a loss of grandfathered status:

- The elimination of all or substantially all benefits to diagnose or treat a particular condition;

- Any increase in a percentage cost-sharing requirement (such as coinsurance);

- Any increase in a fixed-amount cost-sharing requirement (other than a copayment) (such as a deductible or out-of-pocket maximum) that exceeds certain thresholds (a change that exceeds the maximum percentage/medical inflation plus percentage points);

- Any increase in a fixed-amount copayment that exceeds certain thresholds (a change that exceeds the greater of the maximum percentage/medical inflation plus percentage points or $5, increased by medical inflation);

- A decrease in contribution rate by an employer or employee organization toward the cost of coverage by more than five percentage points below the contribution rate for the coverage period that includes March 23, 2010; or

- The imposition of annual limits on the dollar value of all benefits for group health plans and insurance coverage that did not impose such a limit prior to March 23, 2010

In addition to these six rules depicting plan changes that cause the loss of grandfathered status, the ACA defines that employers who fail to provide a grandfathered plan notice with any statement providing a summary of benefits also lose grandfathered plan status with no opportunity to regain it.

The Departments have the responsibility, under the ACA and other laws, to calculate and communicate annual limits specific to health plans. Under the ACA, they must determine the annual maximum percentage that affects the plan changes listed above in items 3 and 4 above. Additionally, they must determine and disclose the allowable high deductible health plan (HDHP) annual limits necessary to pair with a health savings account (HSA). These HDHP provisions define specific cost-sharing limits for minimum deductibles and maximum out-of-pocket.

Proposed Rule

This proposed rule defines two new modifications regarding the cost-sharing limitations that create the desired compliance and flexibility.

-

HDHP Limits

Cost-sharing changes made to comply with the minimum annual deductible or maximum out-of-pocket requirements, as disclosed annually by the Departments, will not cause loss of grandfathered status

- Increases to fixed-amount cost-sharing requirements that otherwise would cause a loss of grandfather status would not cause the plan or coverage to relinquish its grandfather status, but only to the extent the increases are necessary to maintain its status as an HDHP under section 223(c)(2)(A) of the Code.

-

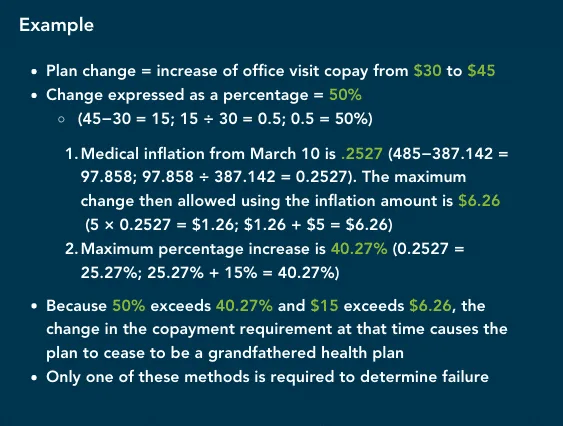

Maximum Percentage

Increases in cost-sharing measurement change will include either the current medical inflation or the premium adjustment percentage minus one, expressed as a percentage, plus 15 percentage points. The greater of these would cause a loss of grandfathered status. [NOTE: Changes made prior to the effective date of the final rule will not be able to use the new premium adjustment percentage when determining grandfathered plan status.]

- Increases to fixed-amount cost-sharing requirements for grandfathered group health plans and grandfathered group health insurance coverage that are made effective on or after the effective date of the final rule, would cause the plan or coverage to cease to be a grandfathered health plan, if the total percentage increase in the cost-sharing requirement measured from March 23, 2010 exceeds the greater of (1) medical inflation, expressed as a percentage, plus 15 percentage points; or (2) the portion of the premium adjustment percentage, as defined in 45 CFR 156.130(e), that reflects the relative change between 2013 and the calendar year prior to the effective date of the increase (that is, the premium adjustment percentage minus 1), expressed as a percentage, plus 15 percentage points.

Nothing in the rule will allow grandfathered status to be restored if it was already lost prior to the effective date of the rule.

Next Steps

Currently, there is no change to the ACA’s grandfathered plan status rules. This proposed rule solicits comments. Public comments are due by August 14, 2020.

Once received, the Departments will review and address all comments. They will then either issue an interim final rule and request further commentary or will issue a final rule to amend the current grandfathered provisions.

Any changes will become effective 30 days after the publication of any final rule. In the interim, employers will still need to follow the current grandfathered status rules.