Terminating Your Retirement Plan: What You Need to Do and How to Tell Your Employees

Author

Article Summary

The health crisis caused by the COVID-19 has created unchartered territory for retirement plan sponsors and plan administrators contemplating potentially long-term changes in the workforce and the financial stability of the plan sponsors and plan participants.

The health crisis caused by the COVID-19 has created unchartered territory for retirement plan sponsors and plan administrators contemplating potentially long-term changes in the workforce and the financial stability of the plan sponsors and plan participants. If your organization has decided to make the difficult decision to terminate your retirement plan, there are a series of tasks and considerations that you must take into account before termination. These include but are not limited to:

- The employer must provide for 100% to all participants at the time of termination.

- Ensure all contributions due are deposited to the plans’ trust before the termination of the plan.

- Re-allocate any unused forfeiture dollars (pay outstanding fees, offset contributions due, or redistribute to participants).

- Consider applying for an IRS Determination letter to solidify your retirement plan’s qualification status at termination. (Optional)

ONEDIGITAL INSIGHT ▼

Employee benefits costs are qualified as “payroll costs” under the Paycheck Protection Program (PPP) and changes made to benefits plan design may impact the amount of relief an employer might receive. Consult with your OneDigital advisor to determine the best course of action for your business.

ONEDIGITAL INSIGHT ▼

Employee benefits costs are qualified as “payroll costs” under the Paycheck Protection Program (PPP) and changes made to benefits plan design may impact the amount of relief an employer might receive. Consult with your OneDigital advisor to determine the best course of action for your business.

ONEDIGITAL INSIGHT ▼

Employee benefits costs are qualified as “payroll costs” under the Paycheck Protection Program (PPP) and changes made to benefits plan design may impact the amount of relief an employer might receive. Consult with your OneDigital advisor to determine the best course of action for your business.

In addition to these steps, the IRS has developed a checklist to aid in properly terminating a Retirement Plan. Reference the checklist here: Terminating a Retirement Plan.

Employee Notification & Guidance

One of the additional steps to terminate a Qualified Retirement Plan is the requirement that you notify participants of the impending termination. The notification must be provided to participants no later than 60 days prior and no sooner than 90 days before the desired termination date. As an additional notification requirement, plan sponsors must provide also provide the 402(f) notice, which offers guidance on the individual participant’s distribution or rollover options.

The Rollover Notice will provide affected participants with necessary information on the options and rights available to them concerning how they can maintain the tax qualified status of their retirement accounts by initiating an eligible rollover transaction.

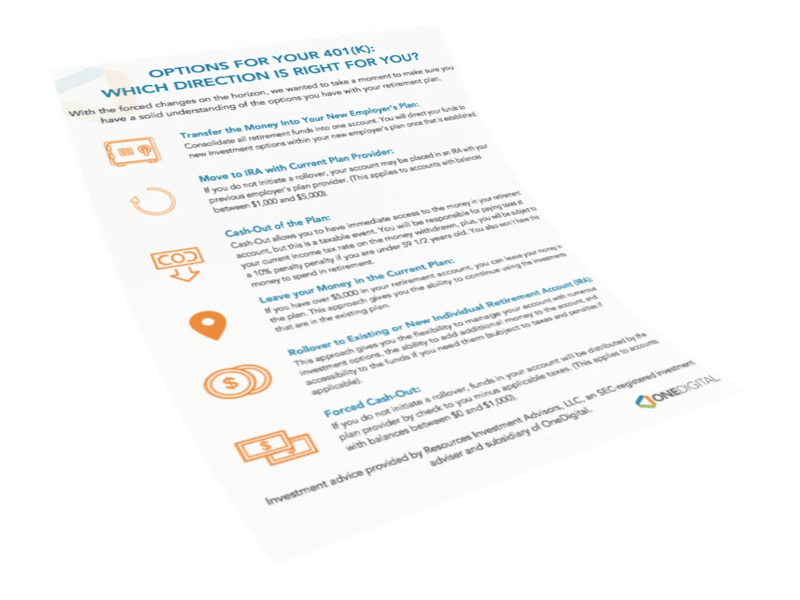

After receiving notification, your employee’s options include:

- Transferring the money to a new employer’s plan

- Moving to an IRA with the current plan provider

- Take a cash-out distribution (10% early withdrawal penalty may apply)

- Leave the money in the current plan

- Rollover to existing or new individual retirement account

Click here for a sample employee communication that details the multiple options employees have with their retirement plans.

Special care should also be paid to plans in which loans are allowed. Under new guidance from the CARES Act signed on March 27th, 2020 and the Bi-Partisan Budget Act signed in early 2018, participants may have increased flexibility on how they can avoid a loan default due to the sudden termination of a retirement plan. Participants with outstanding loans at the time of termination should seek individual advice specific to their own circumstances on how best to avoid a loan default.

Employees should always consider the long-term importance of saving for retirement as well as the short-term tax implications of distributing their funds as opposed to rolling them into a new employer’s plan or an IRA.

For many participants, this may be a crucial fork in the road for their retirement planning future and hastily made decisions under financial stress and a lack of proper guidance can create a significant negative impact on their future retirement income. Plan fiduciaries must consider that, other than the purchase or sale of a home, in many cases, this decision may be one of the most significant financial transactions made in an employee’s lifetime. Plan sponsors and fiduciaries should ensure that participants have access to guidance and all critical information available pertaining to this unique circumstance.

Keep in mind a plan cannot be formally terminated until the last of the assets have been distributed. Consider having a financial advisor available to help your employees make this important decision or take the necessary steps to evaluate and select an IRA provider to force the assets out of the plan with proper notice.

For more information on the important steps businesses should take in the wake of the coronavirus, visit our OneDigital Coronavirus Advisory Hub, or reach out to your local OneDigital advisory team.

Note: Please consult with your plan advisor or plan provider regarding the rules and guidelines specific to your organization and your retirement plan. All the options included on the sample document may not apply to your plan.