How Aggregating Specific Deductibles Affect Stop Loss Strategy

Author

Article Summary

Aggregating specific deductibles (ASDs) can lower stop loss premiums by shifting more risk to employers, offering flexibility in funding strategy. However, savings are not guaranteed, and employers may face significant financial exposure if claims exceed expectations. A data-driven approach is essential to balance cost, risk, and long-term plan performance.

Self-funding provides employers with greater control, flexibility, and the potential for cost savings. However, it also introduces risk, particularly from large individual claims and total claims exposure.

To manage this risk, employers rely on stop loss protection. Individual stop loss safeguards against catastrophic claims, while aggregate stop-loss protects against the cumulative impact of total claims over time.

As healthcare costs continue to rise, employers are looking for more strategic ways to balance cost control with risk exposure. One approach that often enters the conversation is the aggregating specific deductible (ASD).

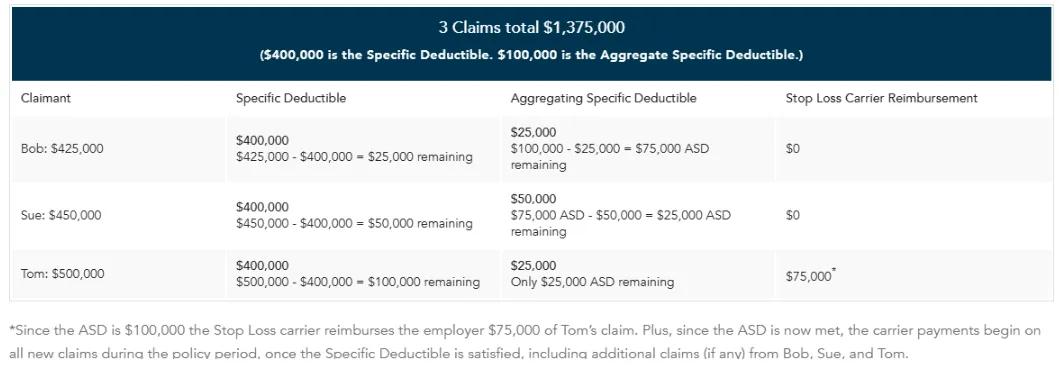

The graphic below illustrates how an ASD works when there is a stop loss reimbursement. Please note an ASD can apply to one or more members depending on the severity of the claims.

What an Aggregating Specific Deductible Actually Does

An aggregating specific deductible allows employers to take on additional risk in exchange for lower stop loss premiums. Instead of increasing the specific deductible for each member, the employer accepts a defined level of additional aggregate risk across claims.

In many cases, this can reduce upfront premium costs. A stop loss carrier may offer a dollar-for-dollar premium credit, meaning a $100,000 ASD could reduce premium by the same amount.

However, the outcome is not guaranteed. If claims exceed expectations, the employer may fund that deductible during the plan year.

This is where strategy becomes critical. The value of an ASD is not in the initial savings, but in how it aligns with the employer’s overall risk tolerance, claims profile, and long-term funding approach.

Balancing Savings Opportunities with Financial Exposure

An ASD can create meaningful opportunities to offset rising renewal costs. It may also serve as an alternative to increasing the specific deductible, allowing employers to manage how risk is distributed across the population.

In certain scenarios, aggregating specifics can even support a transition to self-funding when carriers lack sufficient data to laser high-risk members.

Where Employers See the Upside

- Premium savings through ASD credits

A dollar-for-dollar premium reduction can lower upfront costs, with no certainty that claims will exceed the deductible threshold - Alternative to increasing specific deductibles

Helps manage renewal costs without adding financial risk to each individual member - Supports transition to self-funding

Can enable movement away from fully insured models, especially in limited data or no-laser scenarios

At the same time, the financial exposure can be significant. A large ASD may be funded quickly if a high-cost event occurs early in the plan year, such as a transplant, premature birth, or complex procedure.

Employers must also consider how ASDs interact with renewal provisions. If a plan includes a rate cap, increases to the ASD may still occur alongside premium changes, affecting total financial outcomes.

Not all carriers structure these arrangements the same way. Some may not provide full premium credit, or may cap the reduction based on overall premium levels.

Where Risk and Complexity Increase

- Premium credits may not be fully realized

Some carriers apply partial credits or cap reductions, making it critical to validate contract terms - Potential for early, concentrated financial exposure

A large claim could require the full ASD to be funded in a short period of time - Renewal dynamics can shift expected outcomes

Rate caps and ASD increases may create cost outcomes that differ from expectations

The key takeaway is that savings are not guaranteed, and outcomes depend heavily on contract structure and claims experience.

When an ASD Strategy Makes Sense

The decision to implement an aggregating specific deductible should be based on data, not assumptions.

Benchmarking suggests that most employers can expect between three to six specific stop-loss reimbursements annually based on their size and population. This means there is a strong likelihood that an ASD could be funded during the plan year, even if it reduces upfront costs.

An ASD may be more appropriate for employers that:

- Have higher-than-average specific deductibles

- Are financially prepared to absorb additional variability

- Have a lower probability of large individual claims

- Are seeking to offset premium increases in a controlled way

Healthier groups are often more willing to take on this level of risk, which can lead to more favorable loss ratios and potentially stronger renewal positioning.

Key Strategic Considerations

- High likelihood of funding the ASD

Most employers will experience multiple specific claims annually, increasing the probability of back-end funding - Best suited for higher risk tolerance organizations

Particularly those already operating with higher deductibles - Potential for improved renewal positioning

Healthier groups may benefit from stronger loss ratios and future pricing advantages - Requires a tailored, data-driven evaluation

Employer size, claims history, and financial flexibility all play a role in determining fit

However, the decision should always reflect the employer’s full profile, including size, claims history, financial flexibility, and long-term strategy.

The Bottom Line: Strategy Over Short-Term Savings

Aggregating specific deductibles are not inherently good or bad. They are a strategic lever.

When used correctly, they can help employers manage rising costs and create more flexibility in funding strategy. When misunderstood, they can introduce unexpected financial exposure and misalignment with long-term goals.

The question is not whether an ASD reduces premium.

The question is whether it supports a more informed, balanced approach to managing risk and cost over time.

Build a Smarter Stop Loss Strategy with Data and Expertise

Stop loss decisions should not be made in isolation. They should be grounded in data, aligned with your funding strategy, and tailored to your organization’s risk profile.

OneDigital’s Stop Loss Center of Excellence helps employers evaluate:

- Specific and aggregate deductible strategies

- Claims risk and large claimant exposure

- Stop-loss structuring and carrier alignment

- Long-term cost and risk tradeoffs

Connect with a OneDigital Stop Loss Expert to evaluate your stop loss strategy and determine whether an aggregating specific deductible supports your broader health plan goals.