Lasering vs Premium Adjustments: Employer Guide

Author

Article Summary

As healthcare costs rise, stop loss carriers use lasering and premium adjustments to shift risk to employers at renewal. This blog explains how each strategy works, key trade-offs in cost and predictability, and how employers can evaluate options to make informed, cost-effective funding decisions.

As healthcare costs continue to rise, driven by specialty drugs, high-cost claimants, and increasing volatility at renewal, employers are facing more conservative underwriting strategies from stop loss carriers.

Two of the most common approaches, lasering and premium adjustments, are designed to shift financial risk back to the employer. But while both aim to manage exposure, they do so in very different ways that can significantly impact your total cost and predictability.

For employers evaluating or renewing a self-funded health plan, understanding how these strategies work, and when each is being applied, is critical to making an informed financial decision.

An increasing number of employers are opting for self-funded health insurance plans because they provide greater control, flexibility, and potential for cost savings. However, these plans also come with a heightened risk of financial exposure to large, catastrophic claims.

Employers can reduce the financial risks linked to self-funded health insurance plans by acquiring stop loss insurance, which serves as a protective measure against catastrophic claims and offers a financial safety net for plan sponsors. Stop loss coverage guarantees that once a plan member's claims surpass a specified annual deductible, the insurance carrier assumes financial responsibility for all subsequent payments.

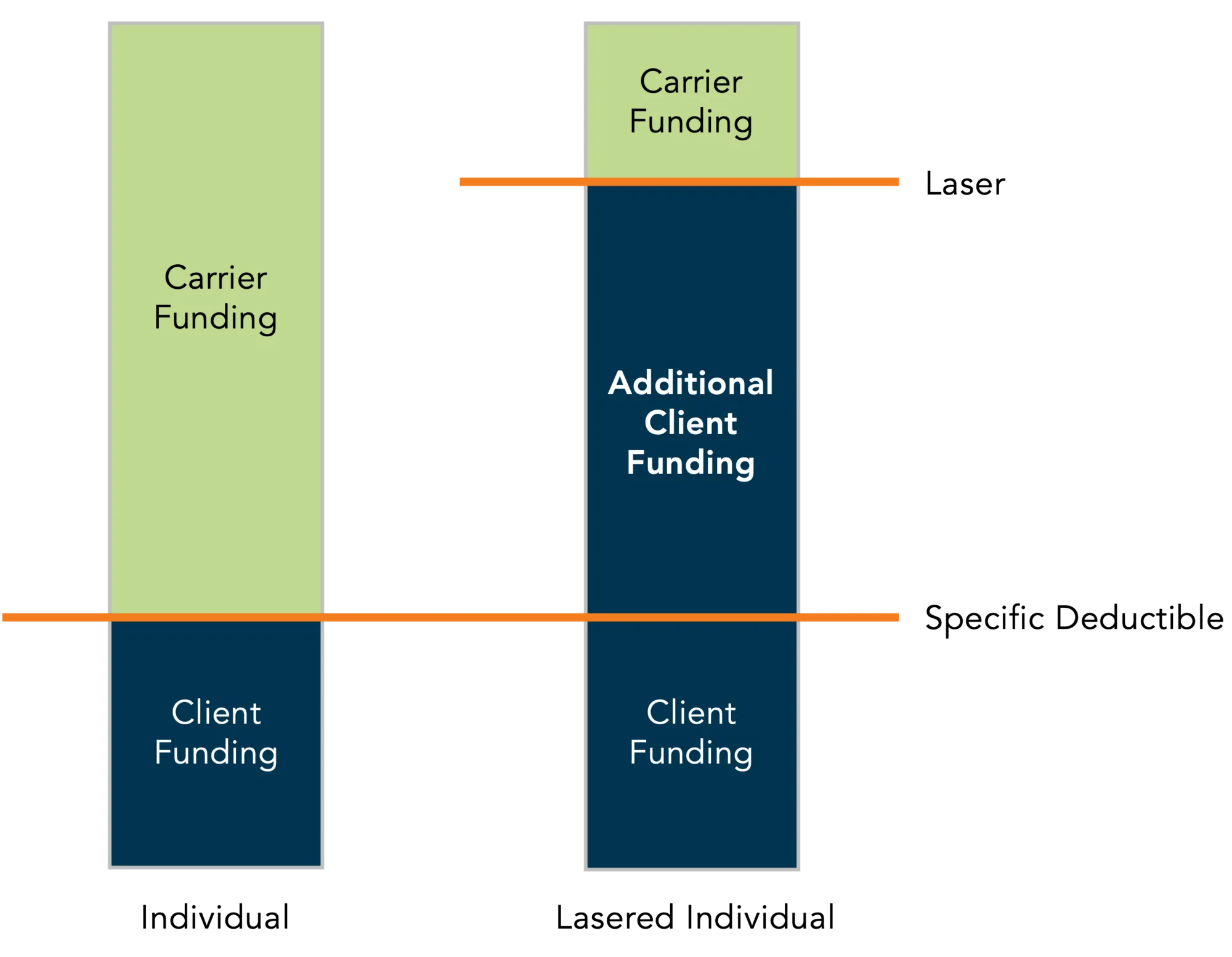

What is 'Lasering'?

Stop loss carriers encounter significant financial risks, leading underwriters to adopt a pricing strategy called 'lasering' to reduce overexposure to ongoing claim liabilities. This method involves modifying the stop loss policy for individual plan members identified as having higher financial risks due to expensive medical and pharmacy conditions.

Lasered plan members are assigned a higher specific deductible under the stop loss insurance plan than their non-lasered peers, meaning that the plan sponsor has a higher financial liability towards these member(s) before stop loss coverage kicks in.

- Straight Laser: Member is assigned a higher specific deductible than the standard case-specific deductible for their non-lasered peers and is not dependent on a specific condition.

- Conditional Laser: Member is assigned a higher specific deductible than the standard case-specific deductible for their non-lasered peers based on a specific condition or treatment.

The advantage of lasering is that it can provide reduced and more stable stop loss renewal premiums. In addition, there is no extra cost to employers if the claims don’t materialize. According to carrier data, only about 25-35% of claims from individuals who have been lasered surpass the specific deductible that would apply to their non-lasered peers. This suggests that the expected financial liability associated with lasering frequently does not materialize.

Conversely, the downside is the potential additional financial exposure relative to a non-lasered renewal premium option and the potential need to fund a significant, large claim in a short duration depending on the condition/treatment.

Premium Adjustments: An Alternative to Lasering

While lasering is one way stop loss carriers manage financial risk, it’s not the only tool in their underwriting arsenal. In some cases, especially when a stop loss policy includes a rate cap and/or a no new laser clause, carriers may instead apply a premium adjustment during the renewal process.

A premium adjustment is an additional load added to the general stop loss premium to account for ongoing, high-risk members. Instead of assigning these individuals a higher deductible, the carrier spreads the anticipated cost across the entire group by increasing the overall premium. This adjustment is typically calculated on a per employee per month (PEPM) basis and can help smooth financial exposure in exchange for a higher up-front cost.

Stop loss underwriters will premium adjust since they cap the allowed ongoing liability each year. These underwriters state that there must be adequate stop loss premium for unknown future risk.

On average, 2/3rds of large claimants for the following year are unknown at the time of the prior renewal underwriting.

One potential advantage of a premium adjustment is that it may result in a lower maximum liability for the plan sponsor compared to a laser, particularly if the lasered individual’s claims end up accumulating to the higher deductible. Because the added cost is known and distributed evenly, it can also make budgeting more predictable.

Lasering vs. Premium Adjustments

However, there are important trade-offs to consider. For one, the premium adjustment scales with enrollment growth, meaning that as the employer adds more plan members, the cost of the adjustment increases. Additionally, because the adjustment is based on projected claims that may never materialize, the employer could end up paying more for risk that doesn’t result in actual costs. Even if the high-risk member leaves the plan or their condition stabilizes, it may still take years of favorable claims experience before the inflated premium begins to decline.

How Employers Should Evaluate These Options

Choosing between a laser and a premium adjustment isn’t just a pricing decision; it’s a risk strategy decision.

In practice:

- Lasering may be more favorable when:

- The likelihood of large claims is uncertain

- Employers are willing to take on some variability for lower fixed costs

- Premium adjustments may be more appropriate when:

- Budget predictability is a priority

- Employers want to limit exposure to large, unexpected claims

- Neither option should be accepted at face value:

- Employers should evaluate alternative funding strategies

- Clinical insights and independent projections should be used to validate carrier assumptions

- Cost containment strategies may reduce or eliminate the need for either approach

The key is not choosing the “default” option, but building a strategy aligned with your organization’s risk tolerance, financial goals, and long-term cost trajectory.

| Option 1: (Laser Renewal) | |

|---|---|

| Premium: | $545,000 (7% renewal) |

| Specific Deductible: | $200,000 |

| Laser: | $400,000 |

| Laser Liability: | $400,000 - $200,000 = $200,000 |

| Total Liability: | $545,000 + $200,000 = $745,000 |

| Option 2: (Premium Adjustment Renewal)* | |

|---|---|

| Premium: | $720,000 (41% renewal) |

| Lasers: | None |

*Premium adjustments may differ based on carrier expense structures.

| Analysis |

|---|

| Difference in Premiums: $720,000 - $545,000 = $175,000 |

| Additional Premium % of Laser Liability: $175,000 / $200,000 = 87.5% |

Why This Matters at Renewal

At renewal, stop loss carriers are actively reassessing risk based on current and projected claims. With rising costs tied to specialty medications, gene therapies, and ongoing high-cost conditions, employers are increasingly seeing:

- Higher frequency of lasers on known claimants

- Increased use of premium adjustments to stabilize carrier risk

- More scrutiny around clinical projections and future liability

For employers, this means renewal is no longer just about rate increases; it’s about how risk is being redistributed within your plan.

Without a clear understanding of these strategies, organizations may unknowingly take on more financial exposure than expected or overpay for risk that may never materialize.

Questions to Ask When Assessing a Laser vs. Premium Adjustment

When choosing between electing a laser or opting for a premium adjustment, it's crucial to develop a tailored strategy that aligns with the unique profile of each employer. The five questions below are an example of a framework that can help with the decision-making process:

- Are there any cost containment strategies to reduce or remove the premium adjustment or laser liability? Can the carriers absorb the additional risk without a need for a premium adjustment or laser?

- What is the nurse's expected cost for the projected ongoing claimants from the carrier? Does this align with the SL COE internal clinical projections?

- Is the employer expected to grow in size? Enrollment growth will inflate the premium adjustment relative to the laser liability.

- What is the probability of lasered member’s claims materializing? Is the underlying catastrophic condition’s cost measurable and predictable based on a clinician review?

- The example above shows the additional premium charged is 87.5% of the laser liability. Does the employer prefer to pay a higher guaranteed, fixed premium when the financial laser liability only materializes in 25-35% of cases?

When weighing lasering vs. premium adjustments, there’s no one-size-fits-all solution. The correct answer depends on your organization’s unique risk profile and financial goals.

As renewal approaches, understanding how carriers are shifting risk is critical to protecting your organization from unexpected costs.

At OneDigital, we help employers model different scenarios, evaluate stop loss strategies, and uncover opportunities to reduce total cost of risk, before decisions are finalized.

Frequently Asked Questions

What is lasering in stop loss insurance?

Lasering is an underwriting strategy where a stop loss carrier assigns a higher specific deductible to a high-risk individual, increasing the employer’s financial responsibility before coverage begins.

What is a premium adjustment in stop loss insurance?

A premium adjustment increases the overall stop loss premium to account for known or anticipated high-cost claimants, spreading the risk across the entire group.

What’s the difference between a laser and a premium adjustment?

A laser concentrates financial risk on a specific individual, while a premium adjustment distributes that risk across the full employee population through higher premiums.

Is lasering or a premium adjustment better for employers?

It depends on your organization’s risk tolerance, financial goals, and predictability of claims. Lasers may reduce fixed costs but increase exposure, while premium adjustments offer predictability at a higher guaranteed cost.

How do stop loss carriers decide between lasering and premium adjustments?

Carriers evaluate known high-cost claimants, projected future risk, plan design, and underwriting guidelines to determine how to manage financial exposure at renewal.

Can employers negotiate or avoid lasers and premium adjustments?

In some cases, yes. Employers may reduce or offset these strategies through cost containment strategies, or alternative funding approaches.