The Internal Revenue Service (IRS) recently announced that it would begin enforcing the Affordable Care Act (ACA) Employer Shared Responsibility rules and penalties in November 2017.

Effective since 2014, the Employer Shared Responsibility rules require an applicable large employer (ALE) to offer minimum essential coverage that is affordable and provides minimum value to substantially all of its full-time employees, or face a potential tax penalty. Prior to its most recent announcement, the IRS had not yet penalized employers for any failures to comply with the rules during the 2015 or 2016 calendar year.

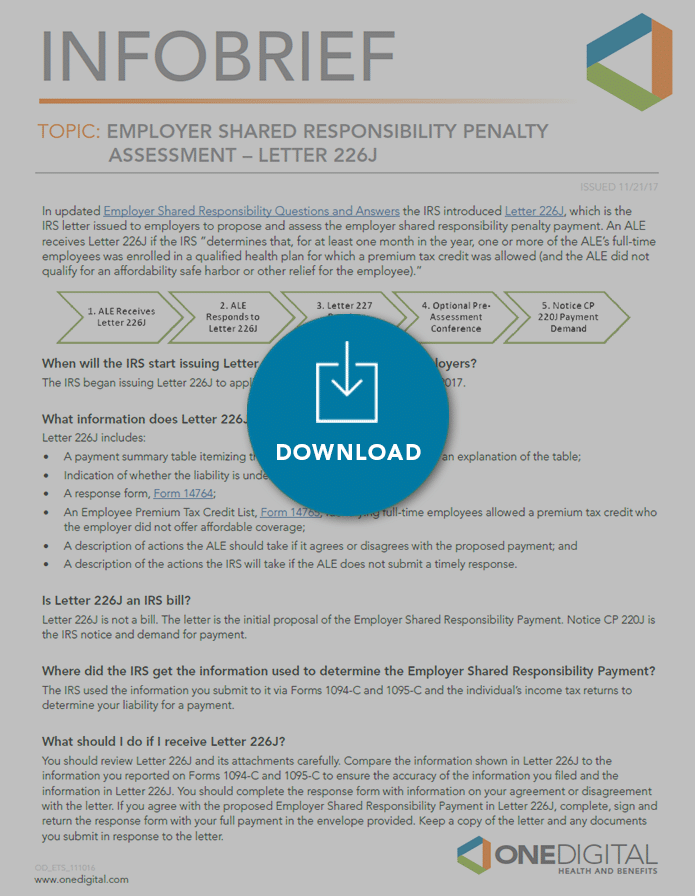

Download The Employer Shared Responsibility Penalty Assessment – Letter 226J

In the updated Employer Shared Responsibility Questions and Answers, the IRS introduced Letter 226J which is the IRS letter issued to employers to propose and assess the Employer Shared Responsibility Penalty Payment.

An ALE receives Letter 226J if the IRS, determines that, for at least one month in the year, one or more of the ALE’s full-time employees was enrolled in a qualified health plan for which a premium tax credit was allowed (and the ALE did not qualify for an affordability safe harbor or other relief for the employee).

What is the process for an Employer Shared Responsibility Penalty Assessment?

When will the IRS start issuing Letter 226J to ALE’s?

The IRS began issuing Letter 226J to applicable large employers in November 2017.

What information does Letter 226J include?

Letter 226J includes:

- A payment summary table itemizing the proposed payment by month and an explanation of the table;

- Indication of whether the liability is under section 4980H(a) or 4980H(b);

- A response form, Form 14764;

- An Employee Premium Tax Credit List, Form 14765, identifying full-time employees allowed a premium tax credit who the employer did not offer affordable coverage;

- A description of actions the ALE should take if it agrees or disagrees with the proposed payment; and

- A description of the actions the IRS will take if the ALE does not submit a timely response.

Is Letter 226J an IRS bill?

Letter 226J is not a bill. The letter is the initial proposal of the Employer Shared Responsibility Payment. Notice CP 220J is the IRS notice and demand for payment.

Where did the IRS get the information used to determine the Employer Shared Responsibility Payment?

The IRS used the information you submit to it via Forms 1094-C and 1095-C and the individual’s income tax returns to determine your liability for a payment.

What should I do if I receive Letter 226J?

You should review Letter 226J and its attachments carefully. Compare the information shown in Letter 226J to the information you reported on Forms 1094-C and 1095-C to ensure the accuracy of the information you filed and the information in Letter 226J. You should complete the response form with information on your agreement or disagreement with the letter. If you agree with the proposed Employer Shared Responsibility Payment in Letter 226J, complete, sign and return the response form with your full payment in the envelope provided. Keep a copy of the letter and any documents you submit in response to the letter.

What if I do not agree with the information included in Letter 226J?

Letter 226J includes detailed instructions for appealing the proposal. If you disagree with the proposed Employer Shared Responsibility Payment, complete, sign, and return the response form no later than the response date shown on your letter (generally within 30 days of Letter 226J). In your response, you should include a signed statement explaining why you disagree with all or part of the proposal and include any supporting documentation.

How will I know if the IRS received my response?

When an ALE responds to Letter 226J, the IRS will provide the ALE with an acknowledgement via Letter 227. There are five different versions of Letter 227 but each acknowledges receipt of the response and outlines any additional action the ALE must take. If, after Letter 227, the ALE still disagrees with the payment, the ALE can request a pre-assessment conference with the IRS Office of Appeals. For more information on this process, see IRS Publication 5.

What happens if I do not respond to Letter 226J?

If you do not respond to the letter by the response date, the IRS will send a Notice and Demand – Notice CP 220J for the Employer Shared Responsibility Payment amount proposed and assessed in Letter 226J. The payment is subject to interest, as well as IRS lien and levy enforcement actions.

Where can I find more information about paying my Employer Shared Responsibility Payment?

The notice will instruct you on how to make a payment. However, you are not required to include the payment on any tax return or make a payment before receiving the Notice CP 220J. The IRS provides options for employers that want to pay in full, are unable to pay in full, or unable to pay at all at this time. For additional information on the collection process and payment options, see IRS Publication 594.

Download The Employer Shared Responsibility Penalty Assessment – Letter 226J

For questions regarding the Employer Shared Responsibility mandate or any of the information above, please reach out to your OneDigital representative today.

Share

Want to learn more about OneDigital?

Connect with a OneDigital expert today.