The Top 4 Social Security Questions Answered

As of 2024, over 68 million Americans receive Social Security benefits monthly, totaling around $1.5 trillion paid out.1

Social Security is a federal program that provides retirement benefits and disability income to qualified individuals. This includes workers, their spouses, children, and survivors. It is one of the most important sources of income for many Americans, especially retirement-aged adults and people with disabilities.

Social Security is complicated as it covers so much for so many different types of situations and there can be a lot of confusion surrounding the various programs. Let’s break down some of the most common questions surrounding Social Security:

1. How Does It Work?

Money for the programs are funded through taxes that employees and employers pay on working income. Subsequently, the money collected through taxes is paid out to current beneficiaries, with any excess that comes in used to fund Social Security trust funds (which are invested in a special version of U.S. Treasury securities).

2. Who Is Eligible?

Retirees

Once you work and pay Social Security taxes for ten years, or 40 credit quarters, you become eligible for Social Security benefits. You can claim and begin to receive benefits as early as age 62 or as late as age 70.

Individuals With Disabilities

Social Security is more than a retirement program as it provides workers benefits when they face a disability that prohibits them from working. Of the 73 million individuals collecting Social Security, 11 million of those are receiving income due to a disability. There are significant requirements that must be met when filing for Social Security for a disability.

Survivor Benefits

A surviving spouse, surviving divorced spouse, unmarried child, or dependent parent of workers who have died (and had enough work credits) can receive benefits on the record of the deceased. In this case, the amount of benefits a family member receives depends on:

- Age of the beneficiary

- Relationship to the deceased

- Earning history of the deceased

3. How Do They Calculate Benefits?

Your Social Security benefits will be calculated based on your primary insurance amount (PIA). Your PIA is the average of your highest 35 years of earnings (adjusted for inflation). Any year with no earnings will count as zero if you have less than 35 years of earnings. To increase your PIA, you can replace a zero or low-income year with a higher one, even if you work part-time through retirement.

PIA is then multiplied by a percentage based on the type and timing of your benefit. For instance, if you were to claim your benefits at your Full Retirement Age (FRA), you would get 100% of your PIA. However, if you were to claim them at an earlier age, the benefits would be reduced by up to 20%.

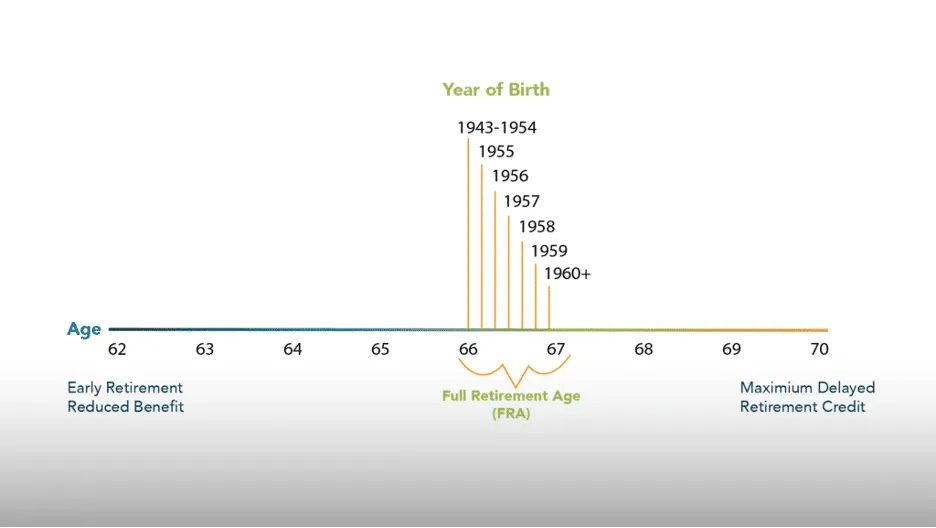

Your FRA is based on the year you were born. For those born prior to 1943, the FRA was 65. Those born from 1943 – 1960 have a Full Retirement Age between 66 and 67 years old as seen in the table below:

Figure 1 - Source: ssa.gov

4. How Do I Apply?

It is recommended to apply three months before you want your benefits to start, and you can do so online, in person at your local Social Security office, or by phone. To apply, you will need to provide necessary personal information such as:

- Your birth certificate

- Social Security number

- Proof of citizenship/lawful status

- Proof of income

- Bank account information

You can create an online account through My Social Security portal to check your earnings and manage your benefits. Ultimately, Social Security is a program that provides income and protection to millions of individuals. Understanding how it works and what it means for you is crucial for making informed decisions about your retirement.

If you would like additional information, watch The Social Security Myth Busting Guide for additional answers. For more information and resources on a variety of financial topics, visit our Financial Academy.

Investment advice offered through OneDigital Investment Advisors LLC, an SEC-registered investment adviser and wholly owned subsidiary of OneDigital.

ID: 00148361